Can You Buy a House With No Job?

It is possible to buy a house if you have no job, but you will need to have other forms of income or savings and be able to effectively demonstrate that you can afford any home loans you want to take out.

Can You Get a Mortgage if You Are Unemployed?

If you are looking to take out a mortgage to buy your house, and you are currently unemployed, you may struggle. Lenders typically look at a borrower’s income or annual salary in order to assess how much money they are willing to loan. Within this, the majority of lenders will ask for a minimum income.

However, some mortgage providers are more flexible than others in how they define “income”. If this is the case, these lenders may accept savings accounts or even benefits as long as you can prove that your monthly income is sufficient to meet payments.

Most traditional banks and financial institutions will only accept full-time employment as a source of income.

If you are unemployed, you will usually need to have a good credit history as well as be able to put down a decent amount of down payment in order to secure a mortgage.

Often, no-income loans, including mortgages, will come with higher interest rates and you will not be able to borrow as much money.

Can You Get a Mortgage When on Universal Credit?

If you are on Universal Credit, you may be able to get assistance with mortgage payments but only if you have been claiming it for more than 39 weeks consistently. However, if you are on Universal Credit at the time of applying for a mortgage, it may affect your eligibility and likeliness of being approved.

How Do You Qualify for a Mortgage When You Are Unemployed?

If you are applying for a mortgage and cannot prove employment, you will need to be able to demonstrate some source of regular income which could include savings. Lenders will also require a good credit history. Regardless of whether you are unemployed by choice, such as taking retirement, or have lost your job, you will need to prove to any lender that you can make regular payments on time.

One way that you may be able to qualify for a mortgage whilst unemployed is by having a co-signer; this might be a relative, spouse or friend. This co-signer will need to be employed or have a high net worth. Co-signers make the mortgage less of a risk for the lender as they are securing the loan with their income and credit history.

Is It Possible To Get a Mortgage on Benefits?

If you are currently receiving benefits, it is unlikely that your lender can use your unemployment income in order to qualify for a home loan. More often than not, lenders require you to prove a minimum of two years of income from a reliable source.

However, if you are receiving benefits it may still be possible to get a mortgage under the right circumstances. This will be contingent on many variables including credit history and alternative sources of income.

If you have a regular source of income, assets or savings, in addition to the money you are receiving through benefits, you are more likely to have your application approved.

For lenders, their biggest concern is whether or not a borrower is able to meet their monthly mortgage obligations. Thus, if the benefits are sufficient to meet payments, and borrowers can demonstrate an otherwise satisfactory financial profile, lenders may indeed approve the mortgage.

Before putting in a loan application, you should check whether the lender accepts benefits as a valid source of income as an unsuccessful application could negatively impact your credit score. Working with a mortgage advisor could help you find the right lender and best deal for your personal circumstances.

Which Benefits Are Accepted by Mortgage Lenders?

Not all benefits will be accepted by mortgage providers and eligibility may vary between lenders. Here are just some of the benefits that mortgage lenders tend to accept:

- Attendance Allowance benefit

- Carer’s Allowance benefit

- Child’s benefit

- Disability Living Allowance (DLA)

- Maternity Allowance benefit

- Pension Credit benefit

- Widow’s Pension benefit

- Working tax credit benefit

Within this, lenders may accept certain benefits but only as a proportion of income rather than as the full amount of proof of income. Certain lenders may have additional specific criteria that you will need to meet before they accept your benefit.

How Can I Demonstrate Eligibility for a Mortgage if I Have No Job?

In order to take out a loan when you are unemployed, you will still need to demonstrate how you will be able to meet repayments and show lenders that you have a solid credit history.

If you are unable to prove employment, you will most likely need to share the following information:

- If you have missed any utility bill payments

- How much credit you currently have available

- If you have previously been declined for loans and how many times

- If you are on the electoral roll

Lenders will only accept mortgage applications for the unemployed if they can be sure that you are able to meet monthly repayments. Demonstrating that you are able to make payments on time and can manage debt in a responsible manner will make you more likely to qualify for a loan.

Can I Buy a House Without a Mortgage if I Have No Job?

Although mortgages are the most common way to purchase a home, there are other ways to purchase a house without the need to take out a loan, including the following...

Cash purchase: If you are fortunate enough to have enough funds available to purchase a house outright, you may be able to save enough for a cash purchase. This is especially possible if you are a two-income household and can live comfortably off a single income for a few years.

In the case that you have no job, you will need substantial savings in order to afford this option or will need to be buying a house with someone who has enough income to support you both for the foreseeable future.

Sell your home to purchase another one: If you are already a homeowner and want to downsize or change living situations, you can sell your existing property and use the profit to purchase another home. This is only really a possibility if you have plenty of equity in your current home.

This can be a great option for those looking to downsize or move to a more cost-effective area where you could get more for your money.

Use an investor: If you are looking to buy a house or property as an investment property, you may find it difficult to secure a mortgage, especially if you have no job.

Getting an investor to cover the expense of buying and renovating the home can be a good option. Many investors will be able to provide cash up front in order to buy the property and pay for any home improvements. Once the property is flipped and sold, you will split the proceeds with the investor.

Can You Add Stamp Duty to a Mortgage?

It is possible to add Stamp Duty to a mortgage by taking out a larger mortgage; however, this may not be advisable as it could impact your loan to value ratio and increase the rate of interest paid.

What Is Stamp Duty and How Does It Work?

Stamp Duty is a type of tax incurred when buying a property or piece of land in the UK. You will pay a different amount of Stamp Duty depending on the purchase price of the property and the property type (i.e. is it residential or not). If you are a first-time buyer, this will also affect the amount of Stamp Duty you will pay.

How Much Is Stamp Duty?

Although there was formerly a Stamp Duty holiday, a government implemented initiative introduced after the impact of the coronavirus pandemic, this holiday ended on 1st October 2021.

Since the holiday ended, any purchases over £125,000 will incur a Stamp Duty with a rate of 2% or more on their property depending on what Stamp Duty band they fall within.

The current Stamp Duty bands are as follows:

- £0 - £125,000 – 0%

- £125,001 - £250,000 – 2%

- £250,001 - £925,000 – 5%

- £925,001 - £1.5million – 10%

- Over £1.5million – 12%

How Is Stamp Duty Paid?

Typically, Stamp Duty is paid by your solicitor on your behalf. This is done as part of the home-buying process, and the home buyer is always the one ultimately paying for the Stamp Duty.

Stamp duty must be paid within fourteen days of buying a property or piece of land.

Can You Add Stamp Duty to a Mortgage?

Yes, in certain circumstances you can add Stamp Duty to your mortgage. However, in general, when you buy a property the only buying cost that tends to be added to your mortgage is the arrangement fee.

That being said, because Stamp Duty is paid after completion on a property, it would be possible to add this to your mortgage. This will depend on whether you can afford to take out a slightly bigger mortgage in order to factor the additional Stamp Duty.

However, the danger of adding Stamp Duty to your mortgage is that this money will also accrue interest over the length of the mortgage term. It may even push you into a higher interest rate bracket. Not only that, but it will affect your loan to value ratio. If you apply for more money, but the amount of deposit you put down is the same, your loan to value ratio will be bigger.

How Can I Add Stamp Duty to a Mortgage?

To get a mortgage to cover the cost of Stamp Duty, you will generally need to apply for a larger loan. However, the danger of this is potentially paying more in the long-run as you increase your monthly repayments and the amount of interest you will pay.

Before deciding whether to add Stamp Duty to a mortgage, it's important to consider how this will impact your mortgage overall, and how this could add to the amount you pay back.

Should I Add Stamp Duty to My Mortgage?

Adding Stamp Duty to your mortgage will increase the overall amount that you need to borrow, and subsequently pay interest on. If you add Stamp Duty to your purchase, the interest rate of the loan will increase and you will also increase your loan to value ratio which could cause you to lose more money in the long run.

Can Your Mortgage Cover Stamp Duty if You Are a First-Time Buyer?

The rate of Stamp Duty will be impacted depending on whether you are a first-time buyer or not, with first-time buyers typically exempt from paying Stamp Duty. For first-time buyers in England and Northern Ireland, there is no need to pay Stamp Duty on the first £300,000 of the property if it is valued at less than £500,000.

What Other Ways Are There To Pay Stamp Duty?

If you want to pay off your Stamp Duty, and are working with a solicitor or conveyancer to help with the purchase, you can usually pay the Stamp Duty directly for them and they can organise everything for you. You can also choose to pay HMRC directly and cut out the middle man.

What you cannot do is pay off your Stamp Duty in instalments; it will need to be paid in full. You also are not able to pay your Stamp Duty on a credit card due to restrictions brought in back in 2018.

Can Mortgage Offers Be Extended?

When you take out a mortgage, there is an agreed mortgage term between lender and borrower; however, this can be extended depending on the circumstances.

Taking out a mortgage can be a long and confusing process for many first-time buyers. Here, Octagon Capital explores exactly what your mortgage offer entails, and if possible, how to extend this past the initially agreed mortgage term.

What Is a Mortgage Offer?

A mortgage offer is confirmation from the mortgage provider that your application has been checked and approved.

You will only receive this confirmation once you have completed the application process fully and provided all the required financial documentation and information about the property you wish to purchase - this can include the following:

- Proof of ID

- Proof of income

- Proof you can afford repayments on the mortgage

- A valuation report on the property

Once you have been given a mortgage offer by the provider, this offer will be valid for a set amount of time - which is typically anything around 3 - 6 months.

How Long Do Mortgage Offers Last?

Mortgage offers are usually valid between 3 - 6 months, depending on the mortgage provider. Mortgage offers will only last for a set period of time, this period typically starting from the moment the offer is issued to the prospective borrower. However, lenders can also start the clock on this offer from the date you first applied for the mortgage.

It's important to know the date your mortgage offer expires, and make sure as best you can that this works for you and fits around your schedule.

Can I Get a Mortgage Offer Extended?

If you are concerned that the house purchase will not be completed within the time frame of the mortgage offer, always speak to your lender first to explain your concerns. Delays are part and parcel of the housing market so lenders should understand if there are any unexpected events that will affect the timeline of purchase. However, the lender is not obliged to extend or re-offer the mortgage.

Depending on the circumstances, it is possible that your lender can offer you a mortgage offer extension. This may be due to personal circumstances, an issue within the housing chain of this particular transaction or at a more global level, such as the coronavirus pandemic.

For example, due to the coronavirus pandemic, many lenders opted to extend their mortgage offers by as much as three months across the UK. Many banks continue to offer extensions so it is always worth checking with your specific provider. Generally speaking, mortgage extensions are reviewed on a case-by-case basis.

What Requirements Are There for a Mortgage Extension?

If you are looking to get an extension on your mortgage offer, your lender will most likely want to see any recent bank statements and payslips. This is in order to check that your financial situation has not changed. Lenders will need to ensure that you are still able to pay back the agreed loan.

Additionally, lenders will require at least a few weeks’ notice in order to see if it is possible to extend your mortgage offer. This will differ between lenders so you will need to check notice requirements directly with your lender.

How Long Can a Mortgage Offer Be Extended?

The length of time that a mortgage offer can be extended will depend on the lender and will usually be evaluated based on an individual case. Lenders will typically take into account the circumstances of the property itself as well as the financial profile of the borrower.

In general, mortgage extensions could be up to a month or more, depending on the situation. For example, one of the UK’s biggest mortgage providers, Nationwide Building Society offers extensions of up to 45 days for those purchasing new-builds and who have come into problems with timings.

How Do I Request a Mortgage Extension?

In order to request a mortgage extension, you have to speak directly to your mortgage lender. The majority of lenders will require at least a few weeks’ notice before extending the mortgage and will need to evaluate many different factors. Lenders are not obliged to provide a mortgage extension, however if your financial situation is unchanged since your initial application, it is unlikely that there will be any issues. The typical mortgage extension will be a month or more.

What Happens if My Mortgage Offer Expires After Exchange?

If your mortgage offer expires between exchange and completion, you should contact your mortgage lender as soon as possible to request an extension.

Typically, your mortgage lender will let you extend your mortgage offer. However, when needed it's important to try and apply for an extension as early as you can, just in case your lender doesn't allow you to extend - giving you more time to make other arrangements.

If you're not allowed to extend your mortgage offer, you may then need to create a whole new mortgage application. This can be done either with the mortgage lender you've initially gone with or another one that's more suitable for your situation.

Can Banks Refuse a Mortgage After Exchange?

Banks and other mortgage providers have the right to refuse to offer a mortgage after the exchange of contracts has happened and, indeed, can withdraw a mortgage application at any point before completion if they have grounds to do so.

Can Loans Affect a Mortgage?

There's so much to consider when applying for a mortgage that it can seem like there's too much to think about. This can especially be the case if you have open loans, and don't know how, or if, they will impact your mortgage application.

We've summed up if having a loan open can impact your mortgage application, and what you need to know about having loans and mortgages at the same time. FInd out more in our Octagon Capital blog:

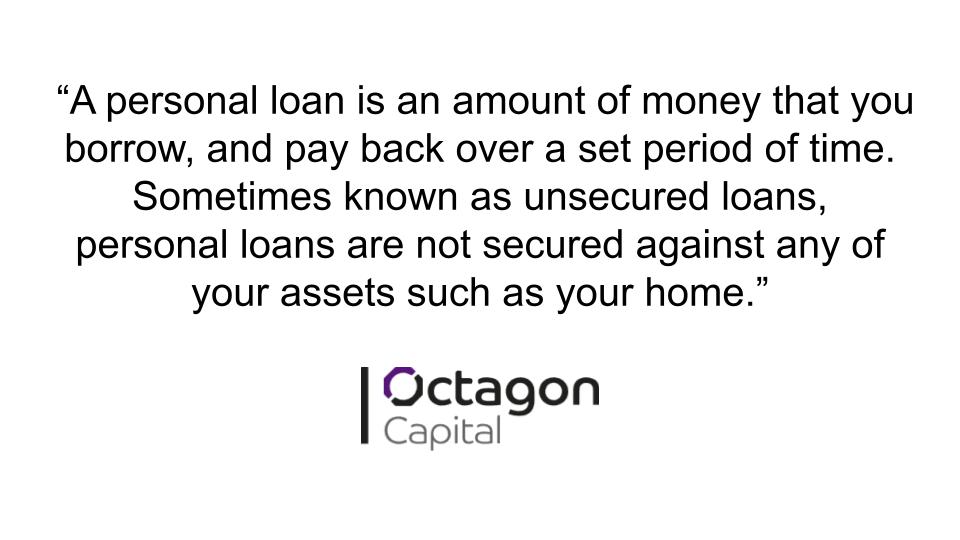

What is a Personal Loan?

A personal loan is an amount of money that you borrow, and pay back over a set period of time. Sometimes known as unsecured loans, personal loans are not secured against any of your assets such as your home.

People choose to take out personal loans for a wide variety of reasons, ranging from help with the rising cost of living, to go on holiday, to fund home improvements, and amongst other things, to pay for vehicle repairs. It's absolutely essential to remember that you should only ever borrow what you know you can afford to pay back, as missed repayments can damage your credit score and result in late fees.

How Do Personal Loans Affect Mortgage Applications?

Mortgage lenders will look at any existing debts when deciding whether or not to approve a mortgage and how much they are willing to lend the borrower.

Before approving a mortgage, lenders will always assess a lender’s credit score in order to determine whether they can meet monthly mortgage repayments.

Therefore any existing debt, including personal loans, will impact a lender’s decision. However, this is not necessarily a bad thing.

If you have existing personal loans but can prove that you are able to reliably meet payment obligations, this could support your case as a reliable borrower. The most important factor will be showing that your income is greater than your outgoing payments, including any loans; this is known as your debt-to-income ratio.

When Will Applying for Loans Negatively Impact Mortgage Affordability?

The timing of your loans can have a negative impact on your mortgage. For example, if you take out a personal loan in the three months leading up to applying for a mortgage, this could negatively impact your credit score and subsequently your chances of being approved for a mortgage.

In general, experts recommend not taking out a personal loan in the six months before applying for a mortgage.

The following loans will impact your credit score and could, therefore, impact your chances of getting a mortgage:

- Personal loan

- Credit card

- Car finance

- Overdraft

- Utility contract

- Mobile phone contract

Applying for any of the following loans will register a mark on your file:

- Personal loan

- Car finance

- Credit card

- Overdraft

- Mobile phone contract

- Utility contract

You should also make sure that any loan searches do not impact your credit rating; the more searches you have with a short amount of time, the less likely you are to be approved for a mortgage.

Can You Take Out a Mortgage if You Have a Personal Loan?

If you have a personal loan, you will still be able to take out a mortgage. However, the most important factor from a lender’s perspective is mortgage affordability and whether a borrower can afford to take out a mortgage on top of any existing debts.

As a borrower with existing loans, it will be your responsibility to prove to the lender that you can repay all of your debts and that you will not be a risk to the lender.

Working with a mortgage broker or mortgage advisor can help you assess the best option for your personal circumstances. These market experts will also be able to recommend lenders who can understand your loan situation and who will be more likely to approve your mortgage application without long-term negative impact on your credit rating.

Could My Personal Loan Improve My Mortgage Application?

In the right circumstances, existing personal loans may even improve your mortgage application.

Having a personal loan which is paid back on time can go a long way in boosting your credit rating and proving that you are a responsible borrower. The more of your loan that you are able to repay before applying for a mortgage, the better you will look to potential mortgage providers.

You can also be strategic but borrowing money through a personal loan and putting the cash in a high interest savings account. This means that you have accrued extra funds which can, in turn, be put forward as a higher mortgage deposit.

Can You Take Out a Loan After You Have a Mortgage?

If you have just received a mortgage approval, it is not an opportune moment to take out a loan. This includes applying for any credit cards or additional finance.

When applying for a loan, you will need to be approved by the lender before fully securing the mortgage. As part of the application, the lender will carry out in-depth credit checks. Therefore, if you take out any further loans or credit after the approval process, this will affect your existing application and can be a red flag for lenders. If the lender believes that this new credit can impact your mortgage repayment, they could even withdraw the mortgage offer.

Even after receiving the mortgage offer, you should not take on additional debt. If you know that you may want to take out further credit after the mortgage application process, you should talk to your lender beforehand to understand the implications and how it may affect your application.

Once you have completed on your mortgage, you may find that you incur extra costs, such as home improvements or furniture, which may require additional funds; thus, you may find yourself in need of credit or a personal loan.

At this stage, there is no real reason why you should not be able to take out a personal loan as long as you can afford the repayments. However, the longer you wait between your mortgage completion and taking out additional credit, the better.

As an alternative, many homeware stores offer 0% finance deals meaning that you may be able to afford these payments without the need of taking out additional lines of credit with interest rates.

Can I Get a Second Mortgage?

If you are looking to buy a second property, applying for a second mortgage can be a good idea. The process is relatively straightforward but you will need to demonstrate that you can meet payments for the second mortgage in addition to your other outgoing payments.

What Is a Second Mortgage?

A second mortgage is a separate mortgage that is taken out on a separate property, leaving the borrower to pay off two mortgages at the same time.

Like a standard mortgage, a second mortgage on a second property will also be a long-term loan in the borrower’s name and held against the property you are trying to buy.

Second mortgages can be used for second properties, a buy-to-let property or a holiday home.

Is It Possible To Have Two Mortgages?

For those looking to buy a second property, be it to rent out or use as a holiday home, they may consider getting a second mortgage. It is possible to have two mortgages at one time.

However, getting a second mortgage can sometimes be more difficult than getting your first mortgage. Banks or financial institutions will often have stricter affordability checks and they will need to assure that you are able to meet payments of both mortgages at the same time, in addition to any other monthly outgoings.

How Is the Process for Getting a Second Mortgage Different?

The process for applying for a second mortgage is more or less identical but there may be stricter affordability checks to make sure you can undergo the strain of paying off two mortgages at the same time.

Is a Remortgage the Same as a Second Mortgage?

A second mortgage is different from remortgaging. When you remortgage, you are either switching your current mortgage deal or switching mortgage lenders. This is usually to save money on the off chance that you find a better mortgage deal.

What Is the Difference Between a Second Mortgage and a Second Charge Mortgage?

A second charge mortgage is a long-term loan taken out to buy a second property but it is secured on the first property. Thus, the new property is secured on the original property. In the case of defaulted payment, second charge mortgages come second to the first charge mortgage.

Usually, in order to take out a second charge mortgage, the borrower will need to have a reasonable amount of equity in a property. This can include the percentage of your existing mortgage that you have already paid off plus any increases in the property’s market value.

Because the property is acting as security, the affordability checks tend to be less strict than for a second mortgage because the loan is less risky for the lender.

Second mortgages, on the other hand, are brand new mortgages secured by a brand new property.

Is It More Difficult To Get a Mortgage if You Already Have One?

Getting a second mortgage is a fairly straightforward process although lenders may be more thorough in their affordability checks. Usually, you will need to demonstrate sufficient equity in your existing home.

It is worth noting that there are usually additional fees incurred if you need to change the status of the mortgage on your existing property.

How Much Can I Borrow for a Second Mortgage?

Like your first mortgage, the amount that you are able to borrow for your second mortgage is likely to be based on your salary, credit history and the amount of equity you have.

You will only be able to borrow against the equity that you already have rather than the full value of the house that you are paying off in your first mortgage.

The better your financial profile, the more likely you are to receive a bigger second mortgage. Thus, a second mortgage may be a good option for those who have already repaid a big chunk of their first mortgage or if the value of your first property has increased substantially due to home improvements or if the area has gone up in value.

Should I Take Out a Second Mortgage?

There are definite advantages to taking out a second mortgage for those looking to buy a second property. By keeping your new mortgage separate from your existing mortgage, you are ensuring that your current home is not at any direct risk. Additionally, if you can afford the repayments, second mortgages can be a cheaper option than a second charge mortgage or a secured loan.

However, taking out a second mortgage can be expensive. Not only will you be paying off two mortgages at once, you will need to have money to pay a second deposit. Additionally, it may be more difficult to get a second mortgage due to the stricter affordability checks.

Things To Consider Before Applying for a Second Mortgage

If you are intending to apply for a second mortgage, there are certain factors you should take into account.

- Reduce your spending - before applying for a second mortgage, cutting back on your spending (including subscriptions and extra bills) can be a good way of improving your financial profile.

- Affordability - make sure that your income can cover the cost of paying for two mortgages over a long period of time in addition to any other financial obligations.

- Paying off your first mortgage - if you are able to, try to pay off as much of your first mortgage as possible before applying for a second mortgage.

- Evidence - prepare proof to show that your income is able to cover two concurrent mortgages.

- Shop around - compare different mortgages to make sure you are getting the best deal available for your circumstances.

Can a Student Get a Mortgage?

Students looking to take out a mortgage for a property are able to do so but will need to consider certain factors including income stream, which lenders are able to provide mortgages and whether the option of a guarantor is available.

Is It Possible for a Student To Get a Mortgage?

You can get a mortgage as a student and there are many providers across the UK willing to offer mortgages to students aged 18 or over. However, you should always consider your financial situation and how a mortgage may impact this.

In general, you will need to demonstrate an exemplary credit score, be able to show a source of income or employment, provide a down payment and show a low debt-to-income ratio. You may also need a co-signer or guarantor.

Those who have received an early inheritance from relatives may benefit from investing these funds into a mortgage. Additionally, those who are studying at a later stage in life (such as postgraduate or mature students) may have access to a greater amount of savings to put towards a mortgage.

Am I Eligible for a Student Mortgage?

In order to qualify for a student mortgage, you will need to meet certain criteria. The two key criteria are the following:

- Down payment - the higher the deposit that you are able to put down on a property, the more likely you are to find a lender who is able to approve your mortgage application. For this reason, it might be better to save for longer in order to have a larger deposit amount.

- Credit history - those with a better credit history will find it easier to get approved for a mortgage. It is possible that as a student you do not have a credit history; if this is the case, there are different ways you can improve your credit before making a mortgage application.

Can I Get a Student Mortgage With a Guarantor?

Applying for a mortgage with a guarantor will mean that the mortgage is more likely to be approved. However, you will need to adhere to certain guidelines. Typically, a guarantor will need to meet the following criteria:

- They are a legal guardian or direct family member

- They are a property owner

- They are a UK resident

In the case of some lenders, there may be a maximum age for the guarantor which tends to be around 75-80 years old.

Depending on the lender, there may also be a minimum deposit requirement which is usually around 15% of the property value. However, in some cases there are lower-deposit mortgages available.

Who Can Provide Student Mortgages?

There are many student mortgage providers across the UK with some of the country’s biggest financial institutions offering suitable mortgage products. Big name banks such as Halifax, Nationwide, Santander, Barclays and Virgin Money all offer student mortgages, just to name a few.

Working with a mortgage broker can help you find the best mortgage to suit your personal circumstances and could also help you to find some of the most competitive deals on the market.

Will My Student Loan Impact My Mortgage?

In some situations, your student loan may impact your eligibility for a mortgage application. However, the most important thing is demonstrating that you have a good financial track record and have sufficient income to meet repayments. Additionally, having a guarantor will make it far easier to apply for a mortgage.

If you are concerned about your student loans, or any other type of loan impacting your mortgage, there are certain things you can do to improve your chances. For example, paying off any outstanding credit card debts can help to improve your credit rating. Additionally, being able to offer a higher deposit (using savings or inheritance) can strengthen your case. Finally, the stronger your guarantor’s financial profile, the higher your chances are of being approved for a loan.

Should I Get a Student Mortgage?

There are many advantages to taking out a student mortgage. As with any type of mortgage, entering the property ladder is a life changing step that can benefit you for years to come; getting on the property ladder early will give you a great head start in life.

Depending on where you are looking to buy, a monthly mortgage repayment could work out to be far cheaper than rent and save you money in the long run.

Becoming a home-owner has great potential for the future. For example, if your property increases in value, you could even make money on it in the future either through reselling or charging rent if you choose a buy-for-uni mortgage.

However, buying a property is not a decision that should be rushed into. Becoming a property owner is a big commitment; although you will have flexibility after you finish your studies, for example renting out the property or selling it, you will need to think about this before entering a mortgage agreement.

Additionally, owning a property comes with a great level of responsibility and you will need to keep up not only with your mortgage payments but also things such as maintenance and repairs.

There is an element of risk incurred when using a guarantor for your mortgage; if you are unable to make your monthly mortgage repayments for any reason, the guarantor could risk losing their home.

Are Mortgage Rates Going Down?

There has been a great deal of volatility in mortgage rates in recent months, especially due to the ongoing impact of the Coronavirus pandemic and rising inflation.

Most recently, mortgage rates seem to have been going down but it is debatable how long these drops will last. Here, Octagon Capital explores the latest on the falling mortgage rates, including:

- What’s happened to mortgage rates in recent months

- Whether mortgage rates are actually falling

- The impact of COVID-19 on rates

And more…

Want to get the best rate on your mortgage? Explore ways to get the best rate on your mortgage.

What Has Happened to Mortgage Rates in Recent Months?

Despite expert predictions that inflation would cause mortgage rates to be pushed higher, recent months have seen the mortgage rate fluctuating up and down but with no real changes.

The average interest rate on the 30-year fixed-rate mortgage for November was almost identical to that of October, despite inflation rising to 6.2%.

Are Mortgage Rates Falling?

Looking at the last few weeks, mortgage rates have been falling but by a negligible amount. Data shows that the average contract interest rate for 30-year fixed-rate mortgages decreased from 3.24% to 3.16%.

For a 15-year fixed-rate mortgage, rates dropped by seven basis points to 2.271% APR, according to data from NerdWallet.

In general, the 30-year mortgage has been fluctuating in recent months but has generally demonstrated an upward trajectory, assisted by high inflation rates and rising employment.

The recent drop in fixed mortgage rates is largely due to the omicron variant of the coronavirus.

Due to the falling rates, mortgage application volume increased 5.5% (week on week) according to data from the Mortgage Bankers Association. When mortgage rates drop, it also helps to boost refinance demand.

Increased Demand for Refinance and Mortgage Applications

As a direct result of falling mortgage rates, there has been an increase for refinance demand (7% increase week-over-week). However, when comparing the figures to 2020, it was 28% lower.

Mortgage applications to purchase a home also increased following the drop in mortgage rates. This figure increased by 3% (week-over-week) but was 4% lower than the same week in 2020.

Although the drop in mortgage rates is brief, the increase in mortgage applications and demand for refinancing shows how sensitive the market is to these small changes and how buyers can be brought back.

End of 2021

In the end weeks of 2021, the majority of mortgage experts predicted that mortgage rates will rise again (73% of mortgage experts surveyed in Bankrate’s weekly poll).

18% of experts thought that the mortgage rate would remain steady over these last weeks of 2021 leading up to the end of the year. A small proportion of experts (9%) predicted that the mortgage rates would continue to drop.

The Impact of COVID

As we have seen from the changing mortgage rates in recent weeks, the emergence of the omicron variant has led to market volatility and a small drop in mortgage rates.

The new wave of COVID cases and its variants is thought to put downward pressure on economic progress and mortgage interest rates.

However, according to the Federal Reserve, this economic slowdown is likely to be short-term only. In general, experts are predicting that rates will continue to be volatile but that rising mortgage rates will be the long-term trend going into 2022.

Mortgage Rates in 2022

As we come further out of the pandemic, mortgage rates are predicted to climb throughout 2022. Below are some facts on mortgage rates throughout the pandemic and into the new year:

- Mortgage rates are not set to go down in 2022

- In 2020-2021, the COVID pandemic directly affected mortgage rates

- Mortgage rates during 2020-2021 were ultra-low

- The ultra-low mortgage rates benefited many homeowners and buyers

With inflation predicted to remain elevated, it seems as though short-term interest rates will also be raised in the new year. Experts from the Mortgage Bankers Association and the National Association of Realtors forecast that the 30-year fixed-rate mortgage will rise about three-eights of a percentage point as we enter 2022 leading to a rate of just under 3.5%.

Are Mortgage Advisors Free?

Sometimes - mortgage advisors may be free for customers to use, the advisor getting paid through other means (e.g. commission). However, some may charge for their services. Whether or not you'll have to pay for a mortgage advisor's services will depend upon various different factors, including:

- The product in chosen

- The mortgage value

The cost of a mortgage advisor will also depend on a range of factors. A mortgage advisor should be clear about the cost for their services up-front. If the service is “free”, it is usually because the mortgage advisor will receive a commission from the lender.

Do All Mortgage Advisors Charge a Fee?

Mortgage advisors may or may not charge you for their service depending on the situation. Most often, the product you choose (i.e. the type of mortgage) and the value of the mortgage will affect whether or not you will be charged a fee.

If they charge you a fee, this might be a flat rate or an hourly rate, depending on the mortgage advisor. In addition, it could also be a percentage of the amount you borrow.

Sometimes, the service of a mortgage advisor will be free to you. In this case, the mortgage advisor will be receiving commission from the lender; this is information that will be shared with you.

It is understood in these scenarios that there may be a conflict of interest meaning that the mortgage advisor may be working for the commission from the lender rather than acting in the best interest of the client and opting for the best deal available.

How Do Mortgage Advisors Make Money?

Mortgage advisors will either receive money from the client for their services or will be paid by the lender for any business they bring in on a commission basis.

If payment is received by the client, this could be in one of the following forms:

- A percentage of the amount borrowed

- A flat fee for their services

- An hourly rate

When receiving money from the lenders, there will be an agreed commission rate between the mortgage advisor and the lender. For each client that the mortgage advisor brings to the lender, they will receive a commission.

How Much Do Mortgage Advisors Charge?

Mortgage advisor fees vary between different advisors but typically range between 0.4% and 1%. If they are independent, it is unlikely that they will not charge a fee, however the exact amount will vary.

In general, it is understood that advisors should not ask for a fee that exceeds 1% of your mortgage.

If working on commission, mortgage lenders will typically pay a commission, or procuration fee, of around 0.35% of the loan amount.

A mortgage advisor should be up-front about any and all fees you will be charged for their services. It's important to understand the full cost of using the mortgage advisor before moving forward with their services.

What Does a Mortgage Advisor Do?

A mortgage advisor is a specialist with expert knowledge of the mortgage market. Also known as independent mortgage brokers, these advisors are able to offer impartial advice helping you to compare and contrast different mortgage products to suit your personal needs - a key thing to consider before buying a house.

The mortgage advisor will act as a liaison between the borrower and the mortgage lender. Regardless of whether you are buying a home or refinancing, the mortgage advisor will be able to assist you and assess the best course of action for your personal circumstances.

Their job is to find you the most competitive rates and prices as well as ensuring that the mortgage product is well-suited to the needs of the client. Mortgage advisors can help borrowers determine the size of mortgage they are able to qualify for.

The mortgage advisor is not a lender of mortgage funds but instead sources the mortgage loans from a lender and matches them to the client.

One of the key benefits of working with a mortgage advisor is that they have access to a range of mortgage products across different banks and lenders. This means that the borrower is not limited to the mortgages available at one particular bank.

Does a Mortgage Advisor Do Everything?

It is worth remembering what service a mortgage advisor is able to provide and what services you may need on top of that in order to budget accordingly.

Mortgage advisors offer you advice about what mortgage suits your needs and can recommend different lenders based on your personal circumstances. However, they cannot advise mortgages that are exclusively available if you approach the lender directly.

Can Mortgage Advisors Negotiate Fees?

Depending on the mortgage advisor that you are working with, it is possible that the mortgage fees are not set in stone and there may be the potential for negotiation.

However, there is also sometimes the option to cut out the middleman and for homebuyers to negotiate mortgage rates and fees with banks and mortgage lenders directly.

Can I Pay Back a Bridging Loan Early?

A lender will almost always allow you to pay the loan back earlier than initially planned. Depending on the lender and the circumstances of the loan, you may be charged a fee for paying this back early, known as an early exit penalty. This fee is not always charged, so it’s important to check whether it applies to you before opting for an early repayment.

A bridging loan is intended as a short term means of finance, with regulated companies typically offering a maximum loan period of 12 months, while non-regulated providers will offer up to 24 months. It’s expected that borrowers won’t hold onto the loan for too long, however paying it off earlier than the agreed-upon date is something else entirely.

Here, Octagon Capital answer some commonly asked questions around paying back a bridging loan early, as well as providing a deeper insight into how the bridging loan process works.

Will I Get Charged for Early Repayment?

You could potentially get charged by your lender for early repayment. This is known as an early exit penalty. Some lenders will charge this while others will not – check your loan agreement terms to see if you’ll have to pay this or not.

Borrowers can potentially save money on their interest payments for a bridging loan if they pay back early, as this is charged monthly for as long as it takes for full amount to be repaid. This is why bridging loan lenders may charge an early exit penalty, as they are losing money they would’ve otherwise received from you in interest if you were to have completed the loan to its full term.

Can I Get Out of a Bridging Loan?

You can only get out of the money owed from a London bridging loan by paying what the lender is owed. This can be done via an early repayment of the loan, which, as previously mentioned, almost all lenders will offer.

In contrast to this, if you are unable to pay the loan back for the set repayment date, you can discuss refinancing options with your lender. While you might be able to arrange a more manageable payment plan with the lender when this issue occurs, you’ll still have to pay for the bridging loan you took out.

As a final resort, if a new payment plan can’t be worked out or the lender can’t get hold of you for some months, the property/valuable asset secured on the loan may be repossessed.

How Do Bridging Loans Work?

As the name suggests, bridging loans work by effectively “bridging” the gap between the purchase of one thing and the sale of another.

For example, if you’re looking to purchase a new house, but are waiting for the sale of your current home to go through, you can take out a bridging loan to help temporarily cover the cost of the new home.

Bridging loans are also great for development projects, enabling property developers to access hundreds of thousands or millions of pounds to cover the cost of their projects – with Octagon Capital, you can borrow from £50,000 to £25 million for up to 24 months.

As bridging loans are intended for short-term use, the loans are priced monthly instead of annually, borrowers having the option to pay their interest off each month as it’s charged, or “roll up” the repayments until the end of the loan term.

Below are some key features to expect with bridging loans from Octagon Capital:

- Borrow a minimum of £50,000

- Borrow a maximum of £25 million

- Borrow for up to 24 months

- LTV for regulated – 75%

- LTV for non-regulated – 80% LTV

- Adverse credit histories considered

Open vs Closed Bridging Loans

The repayments for bridging loans can vary depending on whether you have a closed or open bridging loan.

A closed bridging loan is when the loan comes with a fixed repayment date. These types of bridging loans can typically be cheaper than open bridging loans, regarded as less risky. With a closed bridging loan, borrowers may still be able to pay the loan back early before the set repayment date.

An open bringing loan is when the loan does not come with a fixed repayment date. This helps give borrowers more freedom over their payment of the loan. With an open bridging loan, you’ll still have to have an exit strategy to ensure that the loan will be repaid.

How Is a Bridging Loan Different to Mezzanine Finance?

Mezzanine finance requires borrowers to give up equity in their development project or business, whereas bridging finance is secured against property, and is used on a much shorter term. Both types of finance must also pay interest.

Both mezzanine and bridging loans can be a great to help borrowers in certain situations, carrying different levels of risk, eligibility criteria, repayment plans and more. But how precisely do they differ? And which one is best suited to certain situations and circumstances?

Here, Octagon Capital explores the differences between mezzanine finance and bridging loans, and which one works best in different situations and circumstances.

Mezzanine Finance vs Bridging Loan: Which One Is Right for Me?

Mezzanine finance is used more long-term than a bridging loan, requiring the borrower to give up equity either in their development project or business, while a bridging loan is used on a much shorter-term basis, securing a property against the loan while repaying after a few months (the maximum length of time you can take out a bridging loan with Octagon Capital being 24 months).

Mezzanine finance can appeal to lenders as they not only get paid interest back by the borrower, but also get shares, which could potentially be more valuable than a standard repayment by the borrower. Mezzanine finance lenders has been designed to accommodate for ventures that are potentially riskier, with funding available for a range of borrowing periods – from a few months to 10 years.

Mezzanine vs Bridging Loan: Uses

A bridging loan in London can be used for a variety of different purposes, but essentially helps to “bridge” the financial gap for borrower’s between the purchase of a property and the sale or influx of money from somewhere else.

In comparison, a mezzanine loan is used when the borrower can’t afford the loan, or the opportunity is considered too high of a risk for other types of lending. Mezzanine finance can be used to top up an existing loan, to help fund a business project or to help grow a company. While it’s high-risk, the lender could potentially reap the rewards of enormous returns via the shares they’re given.

Mezzanine vs Bridging Loan: Eligibility Criteria

As mezzanine finance and bridging finance operate differently, the eligibility criteria for each type of loan will also differ greatly.

To obtain mezzanine finance through Octagon Capital, applicants will have to meet the following criteria:

- Must offer equity of up to 20%

- Must be based in the U.K., Scotland or Wales

- Must be a limited company

- Adverse credit histories considered

- Both commercial and residential properties considered

Bridging finance in comparison will require applicants to meet the following eligibility criteria:

- Minimum borrowing amount of £50,000

- Must have an exit strategy

- Residential, commercial, mixed properties and HMOs considered

- Must be over 18

- Must be based in U.K., Scotland or Wales

- Adverse credit histories considered

These two types of finance operate differently and will therefore have differing requirements and expectations for eligible borrowers to meet.

Mezzanine vs Bridging Loan: Repayments

Mezzanine finance is paid through both investment/shares in the borrower’s company as well as in cash or PIK (payment-in-kind) interest. Bridging finance is paid either once a sale has gone through on a property or the borrower manages to refinance with something longer term.

The interest for bridging finance is charged per month, however, borrowers have the option to pay this back either monthly or to “roll up” these repayments and pay back the loan in full at the end of the loan term.

How To Find Mezzanine Finance with Octagon Capital

Octagon Capital are a U.K. licensed credit broker, working with a number of reputable mezzanine finance lenders.

![]()

We’ve worked on a big range of projects, and are able to advise you on how best to approach your borrowing needs.

To get started, simply call us on 0333 414 1491 or email us at sales@octagoncapital.co.uk, and speak to one of our dedicated team members to explore your options.